- July 8, 2025

Only three months into the new year and it feels like a year’s worth of events have already happened in the economy and financial markets.

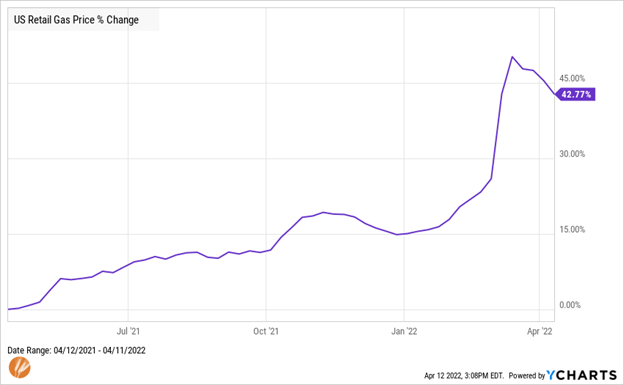

We’ve seen tragedy unfold in Ukraine, inflation persist and further increase, interest rates increase markedly in anticipation of the Fed beginning to raise benchmark rates, and oil prices have increased to near record levels.

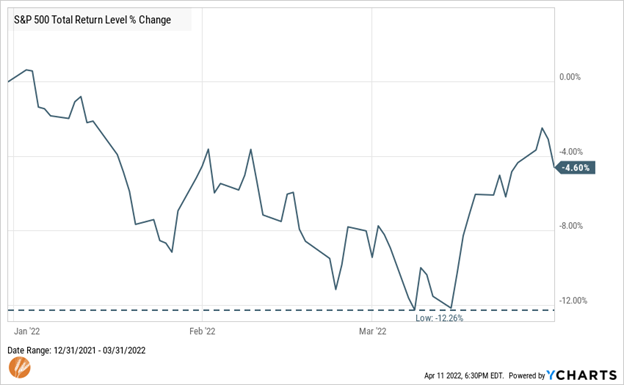

Volatility returned to financial markets after a brief reprieve following the events of 2020. The S&P 500 experienced nearly as many daily changes of at least 1% in the first quarter of 2022 (29) as it did in all of 2021 (35).

The S&P 500 hit its only all-time high of 2022 on January 4th. As compared to 2021, when it achieved this milestone every 3.5 trading days on average. The index bottomed on March 14th at a low of -13% but since recovered substantial ground to close the quarter down 4.6%.

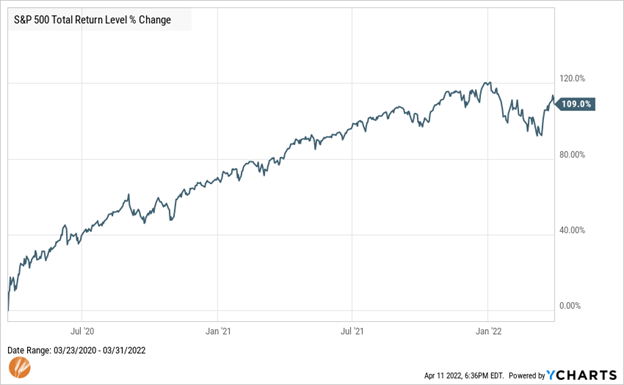

Our last post mentioned that looking at market returns over slightly longer periods provides more perspective. Since we recently had the anniversary of the market’s March 2020 low, it’s worth noting that the S&P 500 has doubled since then. This outcome was difficult to imagine at the time and reminds us of the difficulty of making investment decisions based on market conditions rather than on our financial goals.

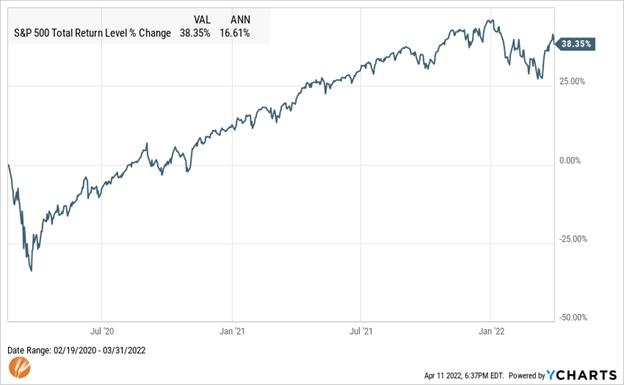

And so we don’t cherry pick results too much, it's worth noting that even since the pre-Pandemic peak stocks have also produced exceptional returns.

The Fed only started raising its benchmark rate in March, but the bond market has been trading rates higher in anticipation of the Fed’s benchmark rate increasing throughout the year. The 10-year Treasury started the year at 1.6% and finished the first quarter at 2.4% – a level last seen in May of 2019. It reached a Pandemic-era low of 0.5% in August 2020.

Higher interest rates have driven down bond prices, but we are collecting higher interest payments on our bond investments. Despite the short-term weakness in bond prices as markets adjust to higher rates, earning higher interest rates into the future is a positive development for return expectations as bond investors.

While it’s nice to earn higher interest on our bond investments, we also pay interest in many cases. An example many can relate to is the 30-year mortgage. Anyone who has taken out or refinanced a 30-year mortgage in the last two years has benefited from historically low rates. But in anticipation of the Fed’s increase in rates combined with their reduction in purchasing mortgages to stimulate that market, the rate new borrowers face has seen a rapid increase from 3.1% at the start of the year to 4.6% recently.

Much of the increase in interest rates is intended to reduce inflation – the likes of which are higher than we’ve seen in quite some time. Running at more than 7% for the last several months is a stark contrast to the barely 2% that has been the norm for many years. Current consensus is that much of the recent inflation has its roots in pandemic-era supply and demand imbalances, has persisted because of exceptionally strong post-pandemic economic growth, and has recently been worsened by events in Ukraine. All seemingly combine to form the perfect storm for supply and demand.

On the afternoon of March 31st after the books were closed on the quarter, the Wall St Journal posted and article with the headline “Stocks Post Worst Quarter in Two Years Despite Strong Finish.” Maybe this was intended to draw a connection with the quarter that ended two years ago when we were in the depths of pandemic uncertainty – a quarter where stocks posted a decline of 20% with a max drawdown of 34%. Sure, it was the first quarter in two years with negative returns, but beyond that held little similarity.

Comparisons like this are often made when risk is perceived to be heightened. Or when a risk that’s been recently forgotten about by the market returns to the forefront. In this case, there is often an assumption that any 5% or 10% decline in stock prices, increase in financial market volatility, increase in interest rates, temporarily higher inflation, or geopolitical event poses meaningful risk to investors.

In our last post we explained that “risk” is when more things can happen than will happen. Many of the passing risks we encounter as investors fall into the category of things that can happen and rarely pose actual risk to our success as long-term investors.

Take financial market volatility as an example. This is the market’s way of weighing all the things that can happen and is a cost we pay in exchange for the returns we earn. More volatility in the short term is a higher cost that is often followed by higher returns, as is the case for stocks. Less volatile short-term assets are lower-cost and we’re paid with lower returns, as is the case for bonds.

These are important distinctions, as focusing investment decisions to mitigate the wrong risk is akin to taking medicine to treat a symptom rather than the underlying ailment. It can lead us astray and potentially derail an otherwise successful long-term investment plan.

But there are important and long-lasting risks that must be addressed for successful long-term investment outcomes. They are risks that are present regardless of the market environment and they can’t be solved with the fashionable investment of the time or by changing an otherwise durable investment strategy.

Risks to the Long-Term Investor

*This section is intended to be a follow-up piece to our last post that can be found here

Permanent loss or impairment of investment capital

One of the primary risks of investing is not the temporary price fluctuations, it is the permanent loss of your capital (I.e., savings). Whether we are thinking about Enron or Lehman Brothers, there are many examples of companies who have gone out of business and their stock has gone to zero. One way to limit the risk associated with a single company’s stock is to invest your savings across many companies (I.e., diversification).

Another element of permanent loss of capital is exiting an investment when the price is down. Every investor expects their investment to go up in value; it is the expectation of being rewarded for accepting some level of risk. Buy low and sell high. As we discussed in our last post, stock prices will fluctuate in the short term; this is normal. However, if an investor were to sell an investment where the market price has declined below what the purchase price was, the investor locks in that loss, making it permanent.

Not keeping pace with the long-term impact of inflation

An investor’s ability to accumulate wealth is tied strongly to their savings rate. An investor’s ability to grow their savings is linked to how those savings are invested. It is a fact that the cost of goods and services increases over time. A dollar tomorrow will have less utility than a dollar today due to inflation. Ella T. Grasso, former Governor of Connecticut, once said “Inflation has... become the cruelest tax, destroying the value of the dollar and adding new costs to every purchase.”

While we are working and accumulating wealth, hopefully our income is growing at a rate greater than or equal to the increased cost of living. Once we have stopped working, and begin to live off of our savings, it is important to ensure our savings are able to keep pace with the long-term impact of inflation or bear the risk of purchasing power eroding over time.

Outliving our resources - "Too much life left at the end of the money"

When we are in our 20s and 30s (at the beginning of our careers), we have a vast supply of human capital – our ability to earn income. As we age, our human capital can become depleted. Everyone will outlive their human capital eventually.

With the proverbial clock ticking on our supply of human capital, we go to great lengths to set a portion of our financial capital (savings) aside during our working years to provide us with an income once we leave the workforce behind. Financial planning and mathematical calculations can help us hone in on how long we need to work, how much we need to save, how our savings will grow and compound over time, and how much of our savings we can spend annually without exhausting our savings.

Upon retirement, investors should be continuously revisiting their assumptions and re-working their plan to ensure their financial capital has the ability to support them throughout their lives. The real risk to a retiree who’s exhausted their human capital is exhausting their financial capital prior to the end of their plan.

Forced errors – changing an investment strategy for the wrong reason such as market conditions

Market conditions change unexpectedly over time and are out of our control as investors. New hot investments will come and go. Investors of sound long-term strategies will see times of confidence in their strategy and times when trendy investments seem like a better choice. These times often coincide with times when markets may be more volatile and investors want to escape the volatility. Action taken in these circumstances comes in different names but can be summarized with the title of “market timing.”

Having a financial and investment plan in place before meeting times like this is the primary mitigator of this risk. The goals and objectives of a plan act as a north star in an environment otherwise filled with smaller stars that can divert our attention. In these circumstances, having a plan allows us to heed Vanguard founder John Bogle’s timeless wisdom when he said, “Don’t just do something, stand there.”

The feeling or perception of riskiness

This element of risk may represent some overlap with other risks. A feeling or perception of excess risk in our investments can erode the confidence needed to stick to the plan when it's most important. It's for this reason that the right amount of risk is one that can be carried out through various market conditions – not only when markets are treating us well. It’s for this reason that the only way to honestly know that amount of risk is with a plan grounded in our goals rather than market conditions, which helps form a connection between our investments and our goals.

Lack of alignment of confidence or perception of the risk in our investments to our goals makes it easier to become susceptible to other risks. When faced with market conditions or hot investments that can divert attention from the most important risks, we become more likely to make a forced error that can lead to permanent loss of capital, which can limit our ability to earn the long-term returns required for our wealth to last a lifetime or longer.

Our last post highlighted evidence that return expectations can take time to materialize. But along the way, we encounter a constant flow of minor risks that, if acted upon, can become one of these five real risks that can limit our ability to earn long-term returns.

After nearly two years of exceptional financial market returns the last few months feel like there is only risk in markets now. However, market conditions we face now only pose a risk to our financial success if we act on them.

Thanks for reading.