- July 8, 2025

After the Great Financial Crisis (GFC) of 2008 and 2009 much was written about how troubling it was that diversification1 no longer worked. This conclusion was drawn since all stocks moved in the same downward direction during the market decline. In recent months, as markets move past the COVID-related market crisis, financial media has reported that it is troubling how low correlations now are among stocks.

After reading this a second time, just to be sure about what I had read, I went back to look at my finance text books to confirm my understanding of diversification. It’s true, diversification works best when stocks behave differently over time.

Why would such a respected publication like the Wall Street Journal report a seemingly incorrect take on diversification? Because for the first time in over a year, markets aren’t being dominated by crises, elections, meme stocks or other topics that produce attention-grabbing headlines. Something so fundamental to investing, that is working better than it has for the last decade or more, is now considered problematic. It’s exactly the opposite of what was considered problematic a decade ago.

This is an indicator that markets are again being driven by things that matter most for long-term investment outcomes – investors’ collective competing outlooks for things like earnings, interest rates, inflation expectations, valuations, risk preferences, and economic growth. There’s nothing interesting left to report on so new problems are made. Quite the welcomed change from most of the last year and a half!

This isn’t to suggest that stocks are going to keep going straight up, interest rates will remain at 0% and risk has left the market. But maybe, at least for a while, financial markets are back to being influenced by relatively boring fundamentals rather than the adrenaline inducing full contact, spectator sport, action movie themes that have recently prevailed.

It’s probably beautiful outside and we’ve all spent too much time in front of a computer screen lately, so I’ll use this opportunity to be brief and not take much more of your time. Afterall, you’ve already graciously kept up with all of this writing over these last many months.

Here are a few quick thoughts on some recent market themes and what they might mean for your portfolio:

Can stocks keep going up?

It depends on the time horizon considered in the question. If the time horizon is three months, a year, or even three years, it’s hard to know. If the time horizon is 10 years, 15 years, or more, then the answer is yes. Thankfully, we invest for 10 years and longer but also plan needs during shorter periods when returns are a bit more random.

Stock prices must be due for a pull-back, right?

Yes. When, by how much, the cause, and the duration are all unknown, though, so as usual it’s best to separate the long-term from the short-term as in the previous question. It’s also important to keep in mind that while pull backs, corrections, etc. are part of investing, they are also temporary.

Recent returns have been great, so does that mean we’re in for lower future returns?

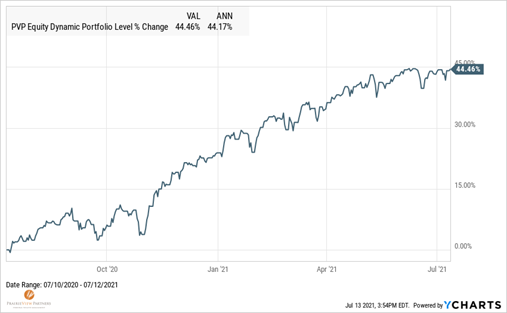

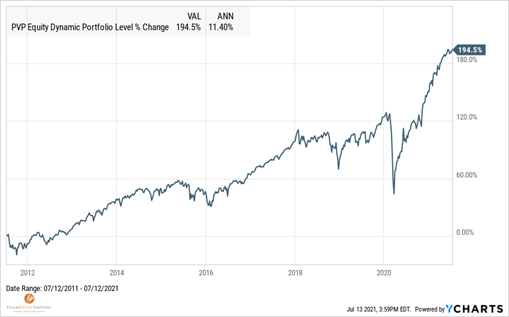

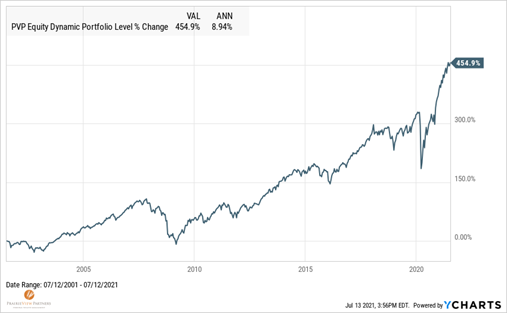

Maybe. Again, it depends on the time frame we measure. If we look at the last year, then, yes, it’s unrealistic to expect 44% returns per year to continue. If we look at the last 10 and 20 years, we see 11% and 9% average annual returns, both of which experienced periods of above and below average returns. Typically, high returns have followed low returns and vice versa. Staying invested through the lower return periods is a requirement to be there for the high return periods.

The average return for all 10 year periods is 9% and the last 10 years falls just in about the top third of all 10 year periods. Definitely strong, but not a statistical outlier.

The average return for all 10 year periods is 9% and the last 10 years falls just in about the top third of all 10 year periods. Definitely strong, but not a statistical outlier.

How many times do you think "market tops" were predicted during the last 20 years?

Should we still buy bonds if we know that rising interest rates will hurt their returns?

Yes. Bonds serve a very important and specific role in most portfolios, which is to provide a stable source of capital, or cash, during stocks’ periodic declines. If done right, and with minimal risk, the most appropriate bonds to serve this purpose will face limited impact from rising interest rates. And on the positive side it means we’ll earn more interest on our bonds in the future.

What might rising inflation mean for my portfolio?

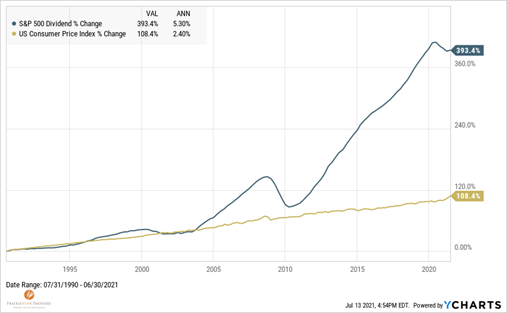

It means that the track record of corporate earnings and dividends growing in excess of inflation over the years and decades remains an important component of investing. It means that common “inflation hedges” are a different way of saying prediction and market timing without using those words and should be avoided accordingly.

Market environments will change from time to time. New risk factors, different drivers of returns, and other variables will prevail and make it feel like an investment plan should change in response. This is rarely, if ever, the case with a well-planned investment strategy. Markets may change but advice doesn’t need to.

Whether during periods of relative calm or heightened volatility, the inclination to do something can be a powerful feeling but, more often than not, is counterproductive. If the last year and a half has reinforced anything when it comes to investing it’s that a steady hand is preferrable to a reactive one.

Speaking of doing something when doing nothing would statistically lead to better outcomes…

In a nod to the recent European Football (soccer) championships that ended in penalty shots, we might be able to learn something from the goalkeepers who dive, seemingly in vain, in attempts to save the shots. A group of researchers in Israel found that strikers shot right down the middle 30% of the time. Goalkeepers on the other hand dove to the left or the right 94% of the time.

The researchers concluded that goalkeepers’ save percentage would roughly double if they simply stayed put2. But diving for the save is more likely to give the illusion of taking action and to make a highlight reel. Recommending action in volatile markets might get one on CNBC, but as with goalkeepers staying put, following a plan is more likely to produce successful outcomes.

Enjoy the summer and thanks for reading.

*Jonathan and I will be back in the “recording studio” next quarter. I’m sure you won’t want to miss it!

- This is an example of the definitions and uses of diversification and asset allocation too often used interchangeably. Diversification, or the ownership of many individual investments in a category, such as stocks, is intended to reduce the risk presented by any single stock, for example, and should not be viewed as a means of protecting against broad market risk. Asset allocation, is the ownership of multiple categories of risk, i.e. stocks and bonds, and most certainly worked as intended for investors in the GFC, COVID crisis, dot-com bust, etc.

- https://mpra.ub.uni-muenchen.de/4477/1/MPRA_paper_4477.pdf

“PVP Equity Dynamic Portfolio” contains broad US and international stock indexes and small cap and value stock indexes. It is rebalanced annually and includes reinvested dividends.