Am I an optimist or a pessimist? I go back and forth. As it relates to the weather today (i.e. sub-zero cold), the evening news, or my hometown sports teams, I generally feel pessimistic. As it relates to the new year, the eventual arrival of Spring, my children’s futures, or long-term financial goals, I generally feel optimistic. What is the difference? For me, it is my time horizon.

Optimism can be defined as hopefulness and confidence about the future or the successful outcome of something.

When it comes to investing, I will argue that to be a successful investor, you must believe in the future and build a plan to maximize your odds of being successful. Nick Murray, author of Simple Wealth, Inevitable Wealth, states “No one can plan for the future – much less invest successfully in it – without believing in that future.”

Regardless of how you generate income, once you have it, you have decisions to make. Should I spend it or save it? Assuming you have enough income to meet your needs and have funds left over, you are faced with another decision to consume the remainder now or set it aside for the future. Your decision to forgo consuming your “extra” income in the near term in favor of saving it for a future financial goal might indicate you are optimistic about your future.

At the very least, you are aware of the future and the need to plan for it. Your ability and discipline to save, be it an emergency fund, a vacation, a down payment on a house, your retirement, or for your children’s education, is a factor 100% within your control… and one that will arguably have the greatest impact on your success or lack thereof.

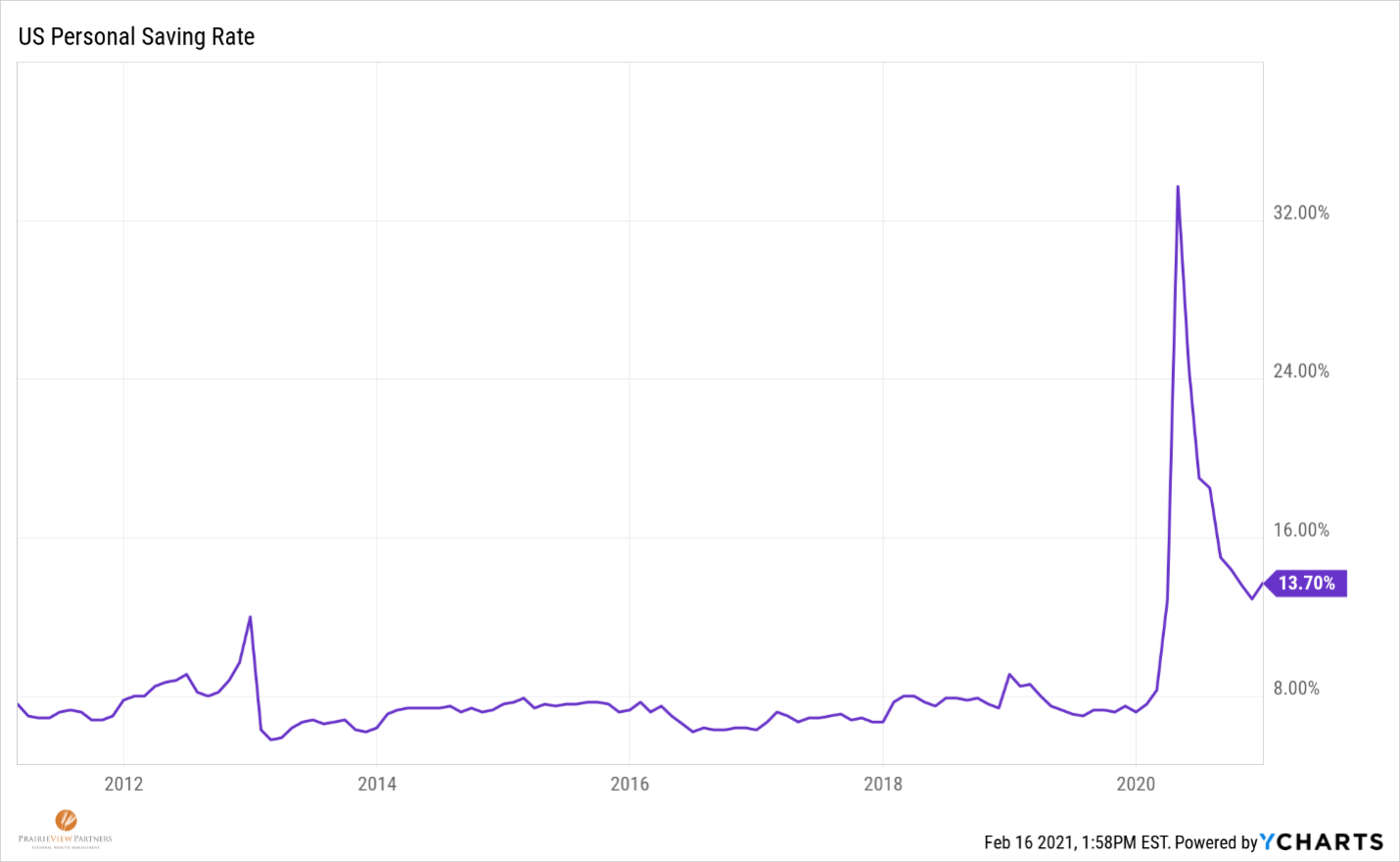

The US Personal Savings Rate at the end of 2020 was 13.40%. The long-term average is 8.76%. While the news cycle paints a pessimistic picture of savers, there is reason to be optimistic.

The US Personal Savings Rate at the end of 2020 was 13.40%. The long-term average is 8.76%. While the news cycle paints a pessimistic picture of savers, there is reason to be optimistic.

“It doesn’t matter whether you make a return of 2 percent, 5 percent, or even 10 percent on your investments if you have nothing to invest.” – Charles D. Ellis

To be an investor, you must first be a “saver”. The decision to save for the future indicates at least some optimism about the long-term. Investing is what savers do with the money they have decided to set aside for long-term financial goals. An investor should not put their savings at risk if they are not expected to be compensated (“paid”) for taking that risk – again, optimism is an important ingredient.

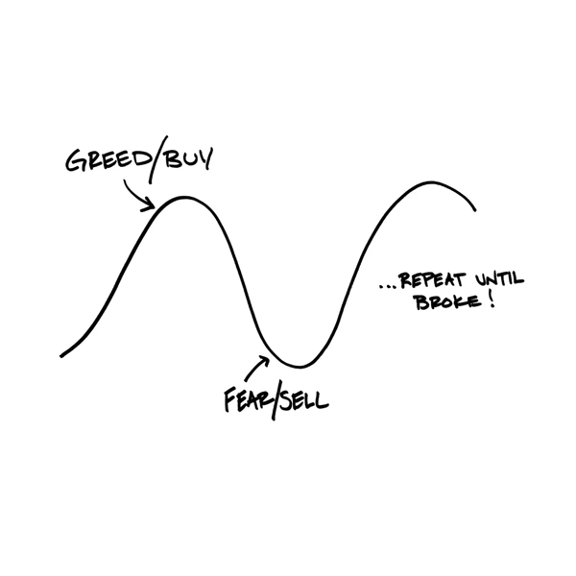

When considering how to invest your savings, meeting your financial goals should not be dependent on anyone’s ability to predict the future. This is where we need to realize that, despite a long-term optimistic outlook, there will times when pessimism rules the day and diversifying our investments will be important.

There are many ways to construct a diversified portfolio, but that is beyond today’s scope. I am more interested in drawing your attention to consistency. Developing and maintaining an investment strategy that will allow you to remain invested during pessimistic times that lead to market drawdowns may be the single most important behavioral factor in your ability to be a successful investor.

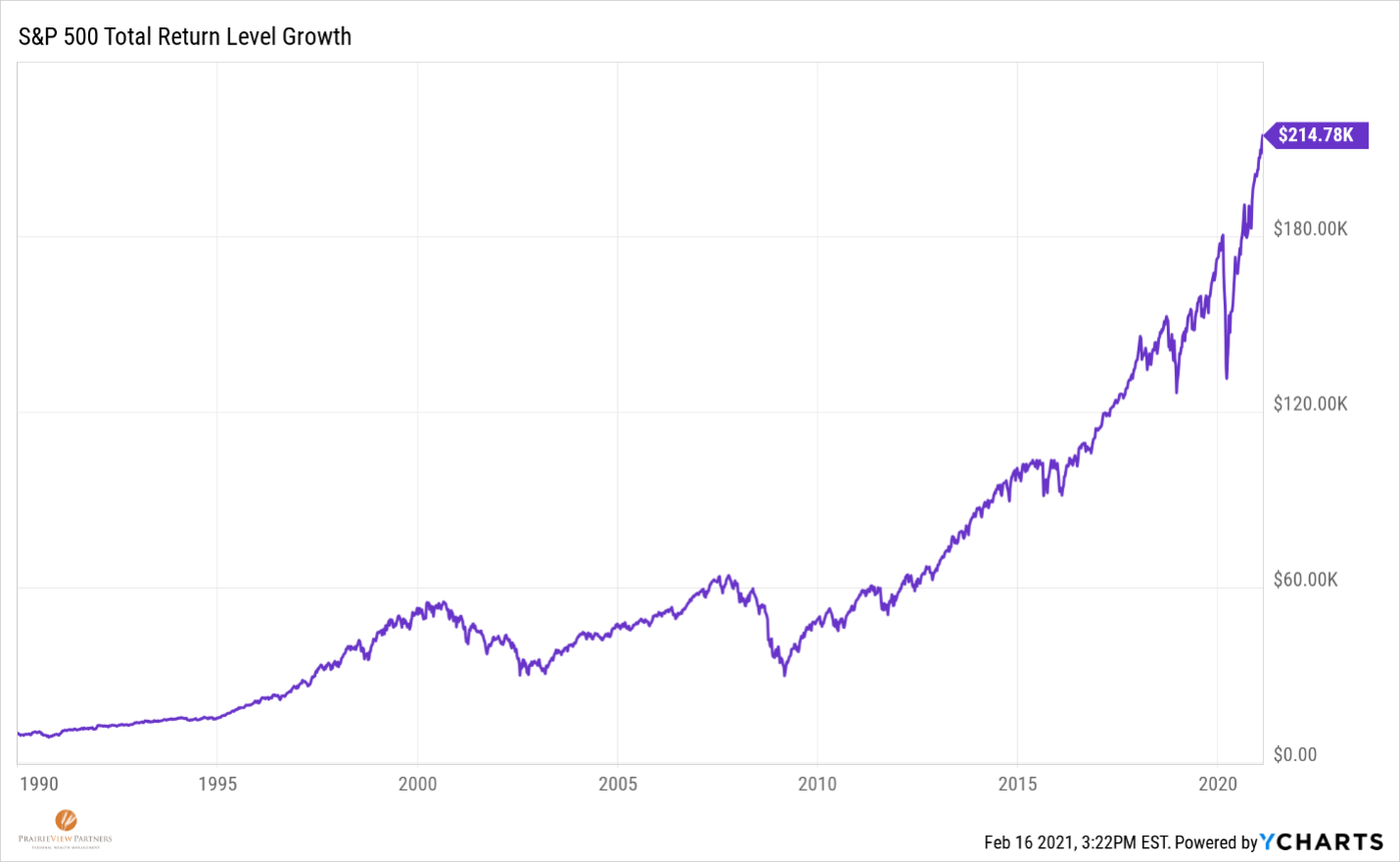

It is often said that time in the stock markets outweighs attempts to time the stock markets and be successful over the long run. History has shown, over the long periods of time and investment cycles, the stock market goes up. For example, if you had invested $10,000 in the S&P 500 Index in 1990 and reinvested all your dividends, your investment would be worth over $214,000 today.

Countless reasons to be short-term pessimistic along the way but long-term optimism delivered nearly 11% annual returns.

Countless reasons to be short-term pessimistic along the way but long-term optimism delivered nearly 11% annual returns.

So, what does all of this have to do with optimism? While historic returns have been great in hindsight, there has been no shortage of reasons to be pessimistic along the way.

As you can see, the growth of the S&P 500 did not go up in a straight line. There were periods in 2000 – 2002 and 2008 – 2009 where markets were down (45%) and (53%) respectively. Last year (2020) the stock market plunged (35%) in 28 days. If you were checking your account balances, watching your evening news, listening to podcasts, or reading investment publications during these periods, it is possible it was a time of great uncertainty for you as an investor. When it comes to our finances, uncertainty can create fear and fear can make us act irrationally; even when we know better.

In the absence of a well-designed investment strategy, it becomes all too easy to be tempted during critical periods to succumb to the pessimism. It might seem easier at the time to sell investments and wait for the right time to get back in. Unfortunately, mistakes like these can set investors back years or possibly never fully recover.

Just like you probably wouldn’t give up on your kids after one bad grade, start rooting for the Detroit Red Wings after another Minnesota Wild loss or pick up and move to Arizona after a couple weeks of sub-zero weather here in the Bold North (ok, maybe you would now), you don’t want your long-term vision for your investments to be clouded by short-term reasons to cause pessimism.

The parts of your life where you are long-term optimistic about reflect your values, goals, and vision of how you want to live your life. A successful saving and investing plan is no different. It needs to reflect your goals, needs, and values in a way that can keep you focused on long-term reasons for optimism and avoid becoming distracted by things that feed short-term pessimism.

Instead of giving up living in a place you otherwise love due to a cold snap, maybe you commit to escaping the cold for a few weeks next winter to help become even more optimistic about your long-term home in Minnesota. When thinking about your long-term investment strategy, you can consider draw downs in the stock prices as an opportunity to rebalance and purchase more stocks “on sale”. Or simply remembering that the portion of your portfolio invested in bonds is intended to help during the more pessimistic periods can help you remember the long-term optimism for stocks.

As investors, it’s so important to take the time to understand our goals, values, and objectives up front That’s what allows us to save and invest during the many periods of pessimism we are sure to encounter. At the end of the day, investment risk is not about the ups and downs of the markets, it is whether your goals are achieved or whether your fall short of achieving your goals.

The last year has provided countless reasons for pessimism – the 24-hour news cycle certainly reminds us of all of them. But the resilience of our capital markets, economy and innovation has proved to be the winning bet every time. Now that is something I have no trouble being optimistic about.

“One of the greatest advantages the individual investor can possess – and the one least available from the 24-hour financial “news” cycle – is long-term perspective.” – Nick Murray

“Investment success accrues not so much to the brilliant as to the disciplined.” – William Bernstein